Where New Zealand’s energy market currently sits (and where it’s going)

What does the future hold for electricity in New Zealand? Is it possible that we will see electricity generated entirely by renewables such as wind, hydro or solar power? Will power be fully automated from generation to consumption? And as consumers of electricity for everything from washing our clothes to powering our new Nissan Leaf, will we be able to remotely control our devices to take advantage of off-peak power periods and save money?

Get ready to geek out on all things electricity.

![]()

How to: New Zealand’s electricity sector

Before we go on a journey to what’s possible, we must first understand how the sector currently works. New Zealand’s electricity grid consists of six distinct parts:

-

Generation – Generation companies generate electricity at power stations, then sell the electricity generated via the wholesale market to retailers. Numerous companies generate power, but 92% of the generation sector is dominated by five companies, all of which also sell direct to customer (and call themselves “gentailers”): Genesis Energy, Contact Energy, Meridian Energy, Mercury Energy and Trustpower.

-

Transmission – Transpower operates the national transmission network, which consists of 11,000 km of high voltage lines (which span from 66KV, 110KV and 220KV). These lines connect power stations with ‘grid exit points’ to supply distribution networks and large industrial consumers (direct consumers). To connect the two islands’ transmission networks, we have a 611 km high voltage direct current link that runs between Cook Strait (called the HVDC Inter-Island, if you’re interested).

-

Distribution – Distribution companies operate 150,000kms of medium and low-voltage lines and transformers which convert power to 240 volts so it’s usable at your average outlet point. There are 29 distribution companies, each serving a set geographic area. These include the likes of Unison, Vector and Powerco.

-

Retail – Retail companies buy electricity wholesale from generators and on-sell it to consumers. Numerous companies sell electricity, including many generating companies, but 95 percent of the retail sector is dominated by five companies: Genesis Energy, Contact Energy, Mercury Energy, Meridian Energy and Trustpower. There’s sometimes a layer in between the retailer and the consumer, and these guys are called ‘Brokers’ who trade electricity on behalf of their clients (usually commercial customers like schools or hospitals).

-

Consumption – Nearly two million consumers buy electricity from retailers. Consumers range from typical households (residential), which consume on average 8–9 MWh per year, to the Tiwai Point Aluminium Smelter (commercial), which consumes 5,400,000 MWh per year.

-

Regulation – New Zealand’s Electricity Authority is responsible for promoting an efficient, competitive and reliable electricity market management of the electricity industry, while Transpower as System Operator manages the electricity system in real time to ensure generation matches demand. Policy and governance is managed by the New Zealand Government and several Crown entities, including the Ministry of Business, Innovation and Employment, the Commerce Commission, and the Energy Efficiency and Conservation Authority.

So, about that Innovation…

The reality is that the rate at which we are currently innovating within New Zealand’s electricity sector is not cutting it (and frankly, this is a little shocking). There’s a few reasons for that…

Welcome to Centralisation-Station

The small number of companies that own a large number of New Zealand’s power plants carry quite a bit of risk. Risk of delays, outages, major malfunctions. And because of our electricity distribution design, that risk is passed down the supply chain, meaning that every issue is absorbed by the recipient, and for the average New Zealander, it means we can’t just speak to a single person about every issue with our power supply (like why we were undercharged by $600 for our winter power bill and we’re only just finding out about it in Autumn).

Electricity is expensive

As consumers, we typically only see the retail end of the supply chain. But before electricity is delivered right to our door, it first has to be generated and travel through a transmission network before being distributed from the grid to the end user at usable voltage levels. The sheer amount of infrastructure and logistics involved in moving electricity is huge. As a result of this, so too is the cost of installing, maintaining and repairing assets like power stations, substations, transformers, transmission lines, links, and the likes.

Add to that, the storage of power on a large scale is economically unviable, so generators have to adjust the generation of power depending on the supply and demand in real time. There’s virtually no margin for error, and companies get penalised if they get it wrong. What you get from this is monopolies (some generators are also retailers) and incentives (to smooth out the peaks and troughs, you might have seen retailers offering incentives for using power during off peak times).

There’s always a vested interest

As with any future market projection, there’s often a fear of the unknown (and the worst case scenario). In the energy sector, things are no different. If new solutions create disruptions in the supply chain, like disintermediation, increased competition or customer evolution, that’s a potential issue for stakeholders. No big business likes unhappy stakeholders.

Looking ahead

The time has come, the walrus said, for the electricity industry to become the well-designed system that us consumers need it to be; to support our needs and our wallets.

The Electricity Authority believes that as a country, we’re well-poised to cope with market disruption. In fact, we were the third jurisdiction in the world to establish a wholesale electricity market in 1996. We’ve also had several major world firsts for the industry, such as half-hour market pricing and internet-based electricity trading. Ka pai!

More than 70% Kiwi of homes already benefit from smart metering, a key enabler to a data-driven electricity grid. That’s 1.5 million meters across the country, and all of the efficiency and environmental benefits that it entails. We also promote a competitive retail environment, helping keep consumer costs down. In the last year the number of companies offering retail electricity has jumped from 22 to 29. To put this into context, five years ago there were only 12.

But we want more than just increasingly renewable or affordable energy. We want to know exactly where our electricity is coming from, how much we’re using and what we’re using it for. We also want to know the impact of our energy usage on the environment, and how we can make informed decisions and positive change.To do this, the whole chain needs to move forward. And the good news is that it’s starting to happen.

Better asset management

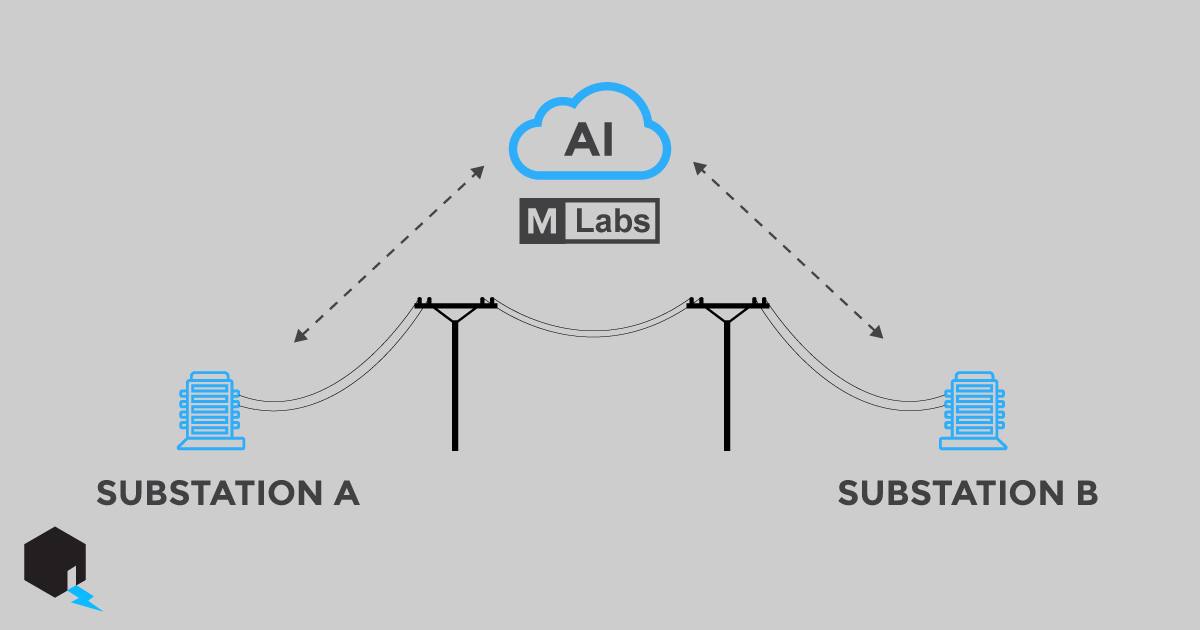

A few years ago, Greymouth Lines company, Westpower, purchased a consulting company and formed Mitton Electronet. The goal was to harness their vast experience in all parts of the electricity supply chain to conduct planning, designing, construction and commissioning of power systems.

Part of Mitton Electronet is currently being accelerated in the Lightning Lab Electric programme based in Wellington. Affectionately known as MLabs (short for Mitton Labs), they’re working on a combined solution using Cloud Computing and Artificial Intelligence to detect and ultimately clear line faults before the current system can even dream of it.

The solution will enable substations to read at a rate of 50 data points per second and create up to 1TB of data per substation per year (across hundreds of substations around the country), that’s a lot of insight to be gained about the lifetime ‘health’ of each ~$30 million asset.

This has the potential to make safe electricity more accessible to the world, especially in emerging markets.

Increased Competition

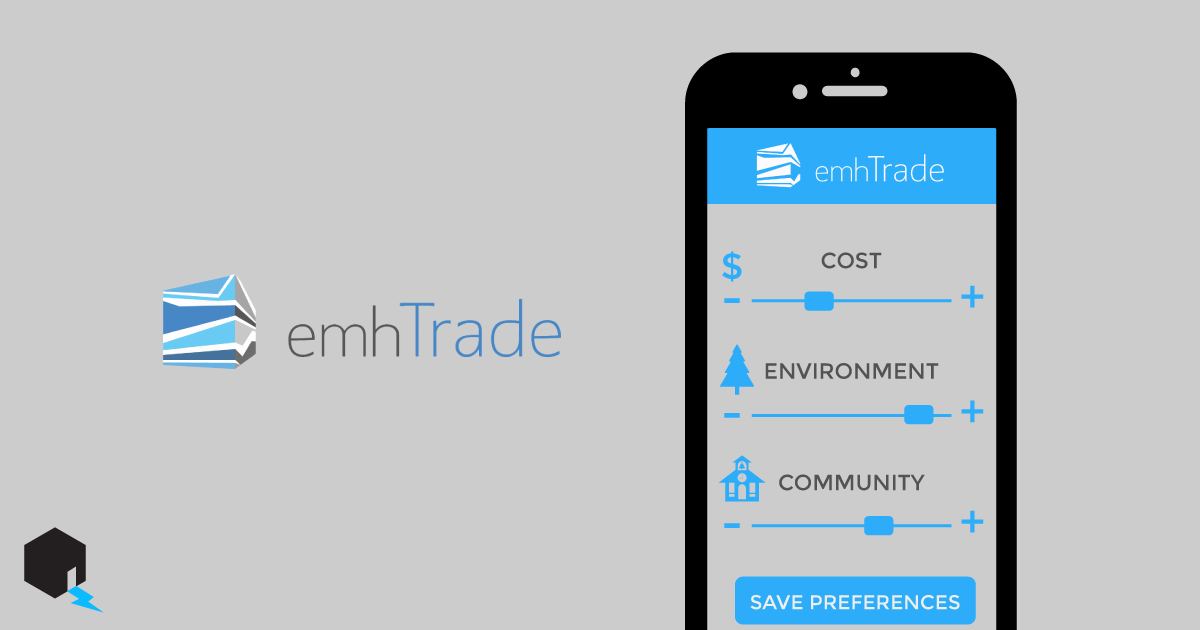

Meanwhile emhTrade, the firm that created New Zealand’s first peer-to-peer electricity platform P2 Power, is working on the next generation of their platform that will allow people to better manage the impact that their power consumption decisions have.

Whether people want their energy to be cheaper, greener, or sourced from locals generating their own solar, the platform will give people a real alternative that allows them to achieve the outcomes that they want.

The team already has a number of smart community programmes in the pipeline including enabling the members of the Blueskin Resilient Communities Trust to create a local, more resilient energy grid.

Smart-Grid Enabler

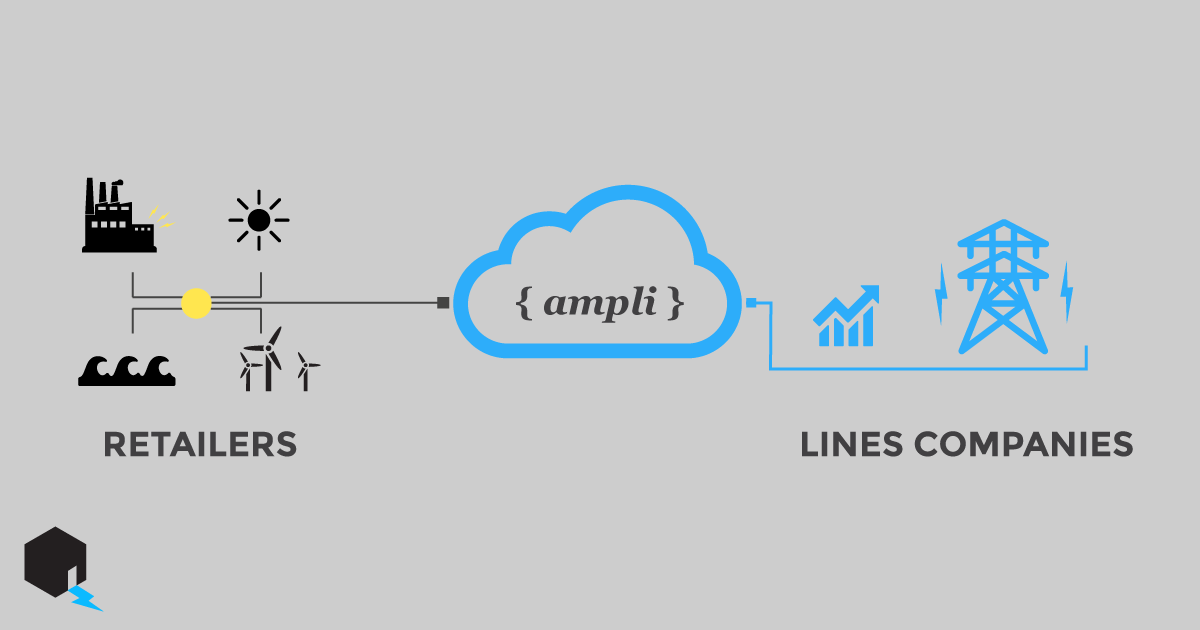

Ampli is a new business intelligence platform leveraging anonymised smart meter data to deliver game-changing tools for the electricity sector. A joint venture between Axos Systems Ltd and Counties Power Ltd, Ampli’s solutions include: tariff design and analytics, network planning and optimisation and outage management applications.

Transparency and Accessibility

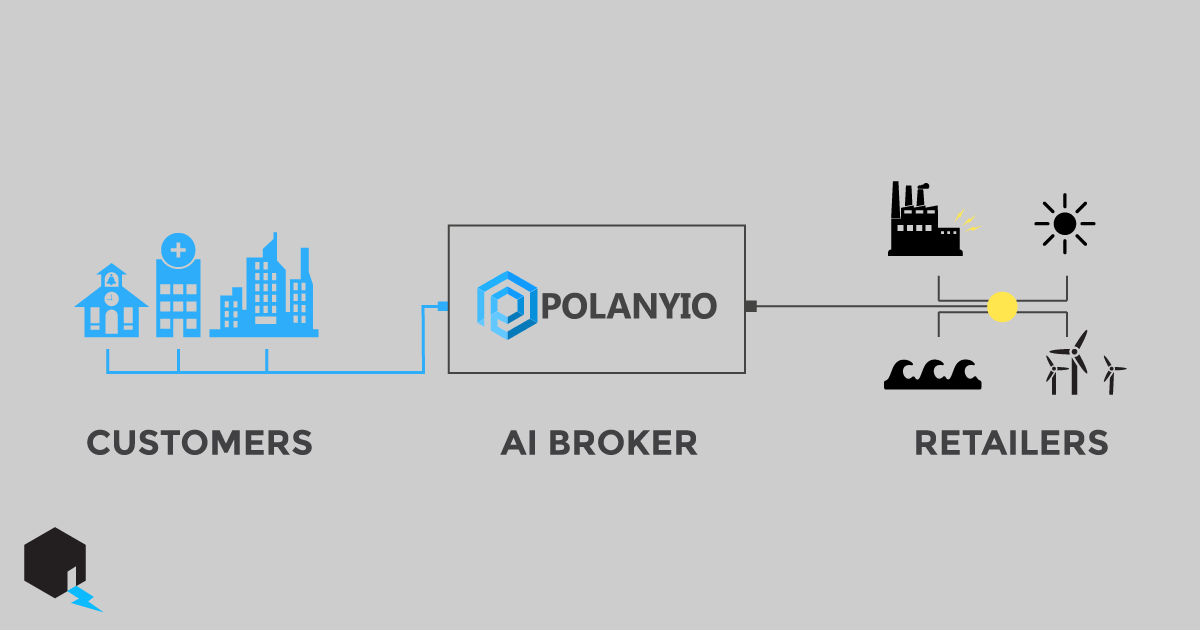

Then there’s Polanyio, the future ‘Xero’ of the electricity market. Their platform combines machine learning with heaps of data to offer some transparent competitive advantages.

It’ll do with electricity brokers what Xero did for Accountants – make the market a whole lot more accessible, and therefore cost effective for business owners (or in this case commercial electricity customers like your local school or hospital).

Where to from here?

The bottom line is that change is coming faster than the electricity sector itself can adapt to and the incumbents need to be more open to working towards innovation. In NZ we are in a world leading position to be able to create, deliver, and ultimately export our electricity advancements.

The first electricity sector innovation accelerator is wrapping up its three-month programme on September 7th and will be assembling in Wellington to discuss progress so far and what steps are needed to fast track it.